Vital Statistics:

| Last | Change | |

| S&P futures | 3002 | 6.5 |

| Oil (WTI) | 60.62 | 0.26 |

| 10 year government bond yield | 2.08% | |

| 30 year fixed rate mortgage | 4.08% |

Stocks are higher this morning after Jerome Powell hinted strongly that the Fed would cut rates at the July meeting. The S&P 500 is at record levels and is flirting with the 3000 level. Bonds and MBS are down small.

Oil prices are rallying as tensions rise in the Strait of Hormuz. Iranian considers the Strait to be its territorial waters, and has been hassling warships going through the area for decades. The latest incident involves a British oil tanker. Persian Gulf tensions largely impact North Sea Brent prices more than West Texas Prices (which most of the US uses).

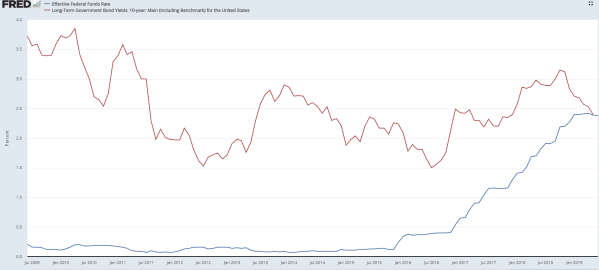

If the Fed is cutting rates, why aren’t yields going lower? Bond yields are higher across the board globally, with the German Bund yielding -26 basis points on hints that the ECB could launch further stimulus plans. The Bund yielded -38 bp last week, so perhaps US bond yields are simply following what international bonds are doing. Don’t forget, the last time the Fed Funds rate was in the 150 – 175 basis point range (May of 2018) the 10 year was about 2.9%. So, the Fed could cut rates 75 bp by the end of the year and we could see yields go nowhere. Look at the chart below, which plots the 10 year bond yield versus the Fed Funds rate:

Initial Jobless Claims came in at 209k last week, which was a touch below expectations. Regardless, the last time we were at similar levels was during the Vietnam War when we had a military draft.

Consumer prices rose 0.1% in June, according to the Consumer Price Index. The core CPI, which excludes food and energy rose 0.3%. On a YOY basis, the headline number rose 1.6% and the core index rose 2.1%. That said, the Fed prefers to use the PCE index, which shows inflation to be lower. The CPI overweights housing compared to the PCE, which is why it shows higher levels.

Jerome Powell’s Humphrey-Hawkins testimony dominated the headlines, but the FOMC minutes also confirmed his outlook.

Participants judged that uncertainties and downside risks surrounding the economic outlook had increased significantly over recent weeks. While they continued to view

a sustained expansion of economic activity, strong labor market conditions, and inflation near the Committee’s symmetric 2 percent objective as the most likely outcomes, many participants attached significant odds to scenarios with less favorable outcomes. Moreover, nearly all participants in their submissions to the Summary of Economic Projections (SEP), had revised down their assessment of the appropriate path of the federal funds rate over the projection period that would be consistent with their modal economic outlook.

Separately, Larry Kudlow emphasized that Trump has no plans to fire Powell. The Fed’s independence from politics makes it highly unlikely he could do so in the first place, however Jimmy Carter did do it to G William Miller, kicking him upstairs to Treasury and hiring Paul Volcker to run the Fed.

The first hurricane of the 2019 Atlantic season looks like it will hit Louisiana.